IFRS CG HK note

IFRS CG HK note

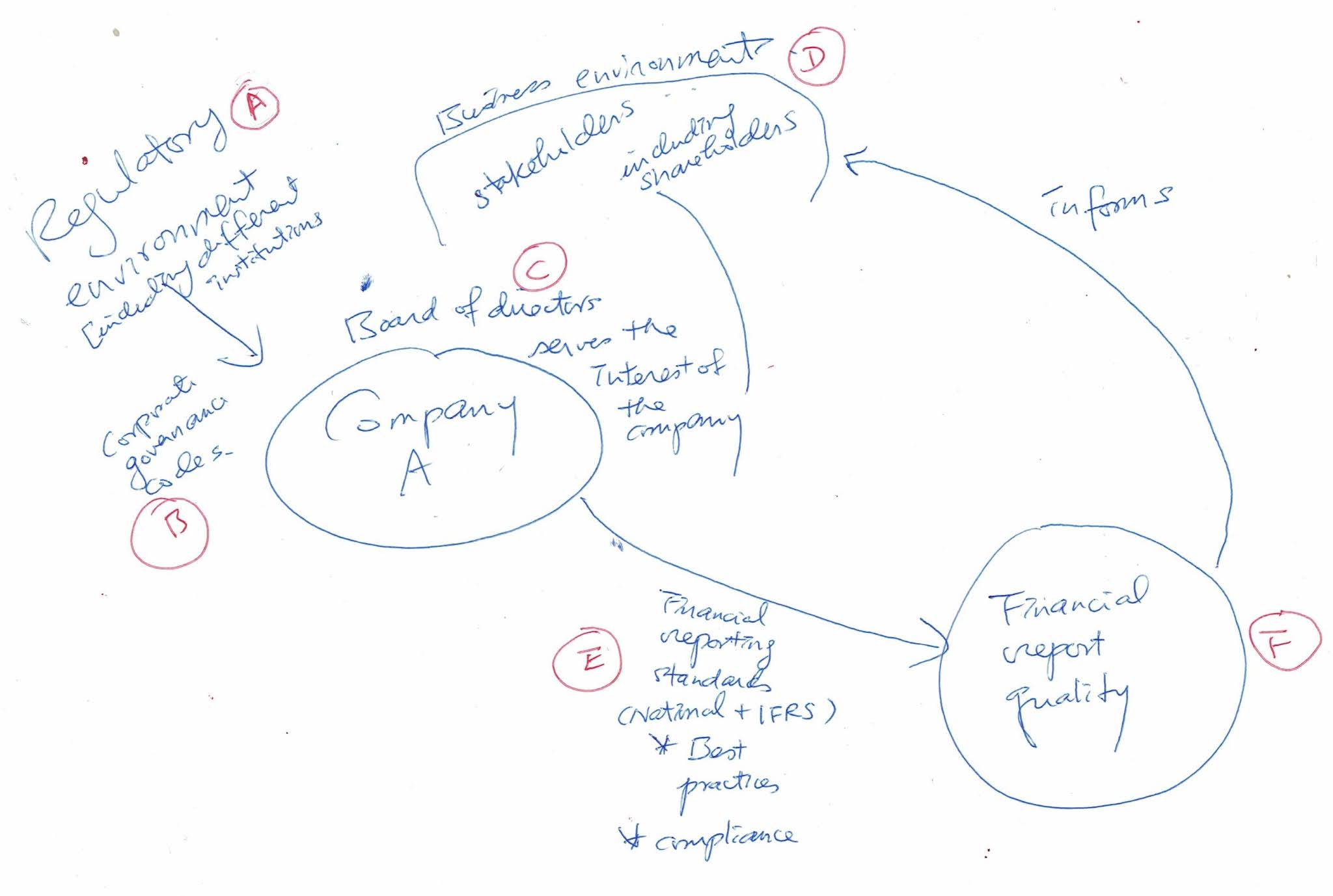

B: corporate governance code

C. Board of directors that serves the interest of the company

D: Business environment, with stakeholders, e.g. shareholders.

E: Financial reporting standards (national and IFRS), as best practices and for compliance

F: Financial reporting quality

Comments

Post a Comment